硅谷Fintech观察④|为什么中国出不了 StripeSilicon Valley Fintech Watch ④ | Why There's No Chinese Stripe

Translated from the Chinese original, first published on WeChat「世像」on July 18, 2026.本文 2026.07.18 首发于微信公众号「世像」。

「为什么中国出不了 Stripe」系列 · 第四篇(终篇)

导读|中国有全世界最好的支付体验,却长不出一家独立的 Stripe。这不是技术差距,更不是人才差距——富途和 Airwallex 早就证明,中国人做得出世界级的金融产品,只不过都得跑到境外去做。差在哪?差在土壤。这一篇给出整个系列的最终答案;文末,还有两条写给普通人的私货。

写在前面

2026 年 6 月,Meta 干了一件耐人寻味的事:它花 9 亿美元投资了印度的金融 App「Cred」,估值约 45 亿;几乎同一时间,把 Cred 的创始人 Kunal Shah 推上了 WhatsApp 全球负责人的位置。

Cred 不是小角色——它服务 1700 万印度人,按笔数算,处理了印度 40% 以上的信用卡账单。但真正好玩的是 Meta 打的算盘:它想把 WhatsApp 做成印度的支付超级 App。可截至 2026 年 5 月,WhatsApp Pay 在印度 UPI 里的份额还只有 0.65%。一位评论者一句话点破了要害——「WhatsApp 在印度的商务里无处不在,在金融里却几乎毫无存在感。」“”

读到这句,任何熟悉中国的人都会心一笑。因为这就是中国故事的镜像,只不过中国早把这一步走完了:当一个超级 App 占满了一个国家的商务入口,独立的金融基建,就很难再从它脚下长出来。

翻译成大白话:印度的 Google 还是 Google,但印度的「摩根大通」正在变成 WhatsApp。你把「印度 / WhatsApp」换成「中国 / 微信、支付宝、美团」,这一篇的题眼就摆你面前了。

前三篇,我走完了一条完整的链条:第一篇,美国券商和资管的解耦早就发生完了,费率归零、无肉可割;第二篇,最聪明的钱掉头去打银行,但打消费侧的大多很惨,真正穿越周期的是卖铲子的人;第三篇,企业支付基建是皇冠,Stripe、Adyen、Airwallex 各自证明了「卖铲子」是一门能做到软件级毛利的生意。

但第三篇结尾,Airwallex 这个华人创立的样本,已经把答案的轮廓剧透了:它能长到 110 亿美元,却要把总部、数据和增长都放到中国之外,甚至要主动跟「中国」这两个字保持距离。

这不是偶然。这一篇,我就来正面回答这个系列的终极问题——为什么这样一层「卖铲子」的基建,在美国能长成皇冠,在中国却几乎长不出来?

我的答案是:中国从来不缺金融科技的人才和产品力——富途和 Airwallex 已经证明了这一点。中国缺的,是孕育 Stripe 这类公司的那片「土壤」。这片土壤由四个变量构成:企业付费意愿、统一大市场、独立分销、并购退出生态。我一个一个讲。

一、土壤变量之一:企业愿不愿意为软件付钱

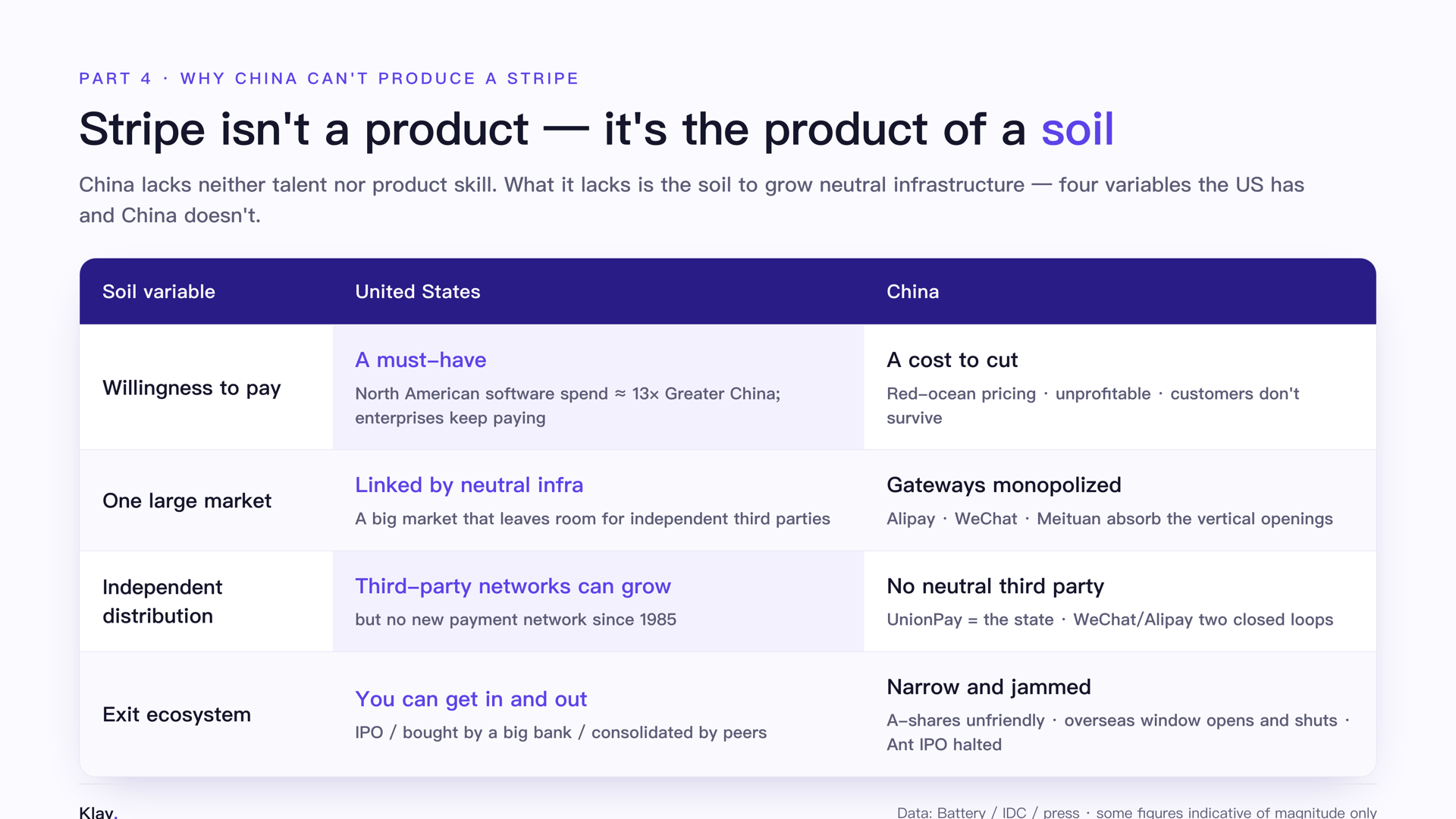

Stripe、Adyen、Ramp 这些「卖铲子的人」,说到底都是被同一件事养大的——美国企业愿意为软件和基建付钱。

这件事有多悬殊?拾象当年引过 Battery Ventures 的一组数据:北美的软件总支出,大约是大中华区的 13 倍(同期美国人均消费支出也差不多是中国的 13 倍)。你要是嫌这个口径旧,看新的:2019 年中国 SaaS 市场只有 30 亿美元,占全球的 2%(IDC);到 2025 年,好几家机构的综合判断还是「美国市场大致是中国的 10 倍左右」。

更要命的是单客户价值。在中国,约 60% 的中小企业对数字化还在观望,真正达到较高数字化水平的只有 3.2%;而中国中小企业的平均寿命,远短于美国——客户活不长,软件的终身价值(LTV)就撑不起来。结果就是中国企业级 SaaS 长年泡在「红海低价、普遍不盈利」的泥潭里,有研究估算中美单客户年付费能力相差近十倍。

(大白话:SaaS=按年付费的企业软件;ARPU=平均每个客户贡献多少收入;LTV=一个客户从头到尾能为你贡献的总价值。一个企业肯不肯为软件持续付钱、能活多久,直接决定了「卖铲子」的人有没有饭吃。)

拾象有句话说得好:「SaaS 是面向白领的机器人。」在美国,软件是企业的刚需消费品,硅谷高速路两边的广告牌几乎全是 SaaS 公司在打广告;在中国,软件更像是「能省则省」的成本项。

这种付费意愿的差距,落到一家公司头上,是惊人的:在美国,一家像样的企业软件公司,单个大客户一年就能贡献几千万美元的经常性收入——数据仓库公司 Snowflake 的大客户 Capital One,一家每年就贡献数千万美元(早期招股书口径)。正是这种「企业肯为软件持续掏钱」的厚土,养出了 Stripe、养出了 Adyen,也养出了上一篇那张表里整整一行的「卖铲子的人」。反过来,当一个市场的企业连软件订阅都要反复砍价、平均活不过几年,这一行的公司就只能去补贴、去烧钱、去抢更下沉的流量——根本攒不出「卖铲子」所需要的那种可重复、又会自己扩张的收入。

没有企业付费意愿,就没有 Stripe 的收入土壤。一家公司可以把支付做得很漂亮,但如果没人愿意为「漂亮的基建」持续付费,它就长不成皇冠——只能去补贴、去烧钱、去抢 C 端流量。这就是中国金融科技的宿命起点。

二、土壤变量之二:统一大市场,却被两个平台吃干净

有人会反驳:中国市场又大又统一,这不正是 Stripe 最好的温床吗?

恰恰相反。中国的「统一大市场」是真的统一、真的够大——但这份统一,是两个超级 App 垄断出来的,不是一层中立基建铺出来的。

看支付:支付宝和微信支付合起来占了中国移动支付的九成以上。看理财:靠着支付宝的分发,余额宝在 2017—2018 年一度是全球最大的货币基金,峰值规模约 1.69 万亿元人民币(约 2680 亿美元)——它证明了中国可以凭空造出一个巨型金融玩家,但赢家是握着用户的平台(支付宝),不是哪个独立的资管创业公司。

最能说明问题的是餐饮 SaaS。在美国,Toast 这样的公司能自己独立长大:它从餐厅 POS 起家,把支付嵌进软件栈里,一边收 SaaS 订阅费、一边收支付抽成,长成了一家上市公司。

这里要纠正一个流传的说法。常有人讲「Toast 在中国之所以出不来,是因为被美团嵌入做掉了」。准确的事实是:美团在中国本就自建了餐饮 POS(智能终端、扫码点单),把这层垂直 SaaS 连同履约、广告流量一块打包自营;它甚至反向出海,组了个团队做了一个直接对标 Toast 的产品 Peppr——结果因为不愿意在海外大战里砸钱,Peppr 已经在美国关停了。一进一出,恰恰说明:在中国,餐饮 SaaS 这层根本不给独立玩家留缝;而超级 App 的打法换到没有流量垄断的美国,又水土不服。

这就是中国「统一大市场」的悖论:市场足够大,但每一个垂直机会——支付、信贷、理财、餐饮 SaaS——都被支付宝、微信、美团用现成的流量在入口层顺手吃掉了。一个独立的 Stripe、一个独立的 Plaid、一个独立的 Toast,在两个超级 App 占满所有入口的格局里,找不到独立长大的那道缝。

再往深一层看,超级 App 之所以能把垂直机会一个个吃掉,靠的不是产品做得多好,而是它手里那个别人没有的东西——十亿级的现成流量。一个独立创业公司要花几年、烧大钱才能获客,而微信、支付宝、美团只要在自己 App 里加一个入口,就能把信贷、理财、餐饮 SaaS 顺手做了,边际获客成本几乎为零。这跟印度的剧本一模一样:WhatsApp 敢想做支付,靠的也是它在印度商务里的统治级渗透,而不是 WhatsApp Pay 本身有多强。当分销可以靠流量「白送」,独立基建那条靠产品和牌照慢慢爬的路,就显得又慢又没必要。这正是超级 App 市场最反直觉的地方:市场越大、平台越强,留给独立中立基建的缝,反而越小。

三、土壤变量之三:独立分销,与「再造一个网络」的不可能

第三块土壤,是独立分销渠道和网络护城河。

上一篇我说过,卖铲子的人真正的护城河不是技术,是分销和牌照。这里有一句可以当全篇题眼的判断:自 1985 年 Discover 诞生以来,美国再没有人在零售规模上建成一张新的支付网络——而且这种情况大概率不会改变。而 Discover 当年能成,恰恰是因为它背靠当时全美最大的零售商 Sears 的分销。

支付的壁垒还体现在牌照的层层嵌套上——有人把它比作「俄罗斯套娃」:打开一家支付公司,里面还套着一家,全靠各地的牌照撑着,连最大的银行也只在约 60 个市场直接持牌。

一句话类比(呼应整个系列):银行的核心系统,是银行的铁镐;而企业支付基建,是整个数字经济的铁镐。谁卖铁镐,谁就站在所有淘金者的上游。

那中国的「铁镐」握在谁手里?答案是:不在任何一个独立的第三方手里。银联是国家队搭的清算网,微信和支付宝是腾讯、阿里两大流量平台各自的闭环。在一个分销入口被国家队和超级 App 占满的市场里,一个像 Stripe 那样「中立、面向开发者、靠企业付费长大的第三方基建层」,缺的从来不是技术,是它赖以生长的那片独立分销土壤。

再说穿一层:美国那条费池链是商业化的——发卡的是商业银行、清算的是 Visa/Mastercard 这种上市公司,每一段都有利润、也都能被一个更利索的第三方撬走一块,Stripe 就是从「收单」这段撬进去的。中国这条链呢?发卡的银行是国有的,清算的银联是国家队搭的,入口是腾讯、阿里各自的闭环——从头到尾,要么姓国、要么姓平台,没有哪一段是留给「中立第三方」的商业费池。这才是比「市场被吃干净」更根子的一层:在美国,费池是块能被撬的商业蛋糕;在中国,它压根就不是一块对外开放的蛋糕。

Airwallex 的解法,本身就是这个结论的证明:它没在中国正面硬刚,而是把战场选在了跨境和海外,用近十年、85+ 张牌照,在中国之外铺了一张网。它甚至要把员工和数据迁出中国,还要回应「中国后门」的质疑——Khosla 的合伙人、同时也是竞品 Ramp 董事的 Keith Rabois 公开指控它的中国团队和中国投资人,使它「可能有义务交出客户数据」,美国参议员已经要求调查。一家带中国基因的全球基建公司,想长大,先得证明自己离中国足够远。

四、土壤变量之四:并购与退出生态——美国把「被收购」也做成了体面

第四块土壤,也是最被低估的一块:有没有一条让创业公司体面退出的路。

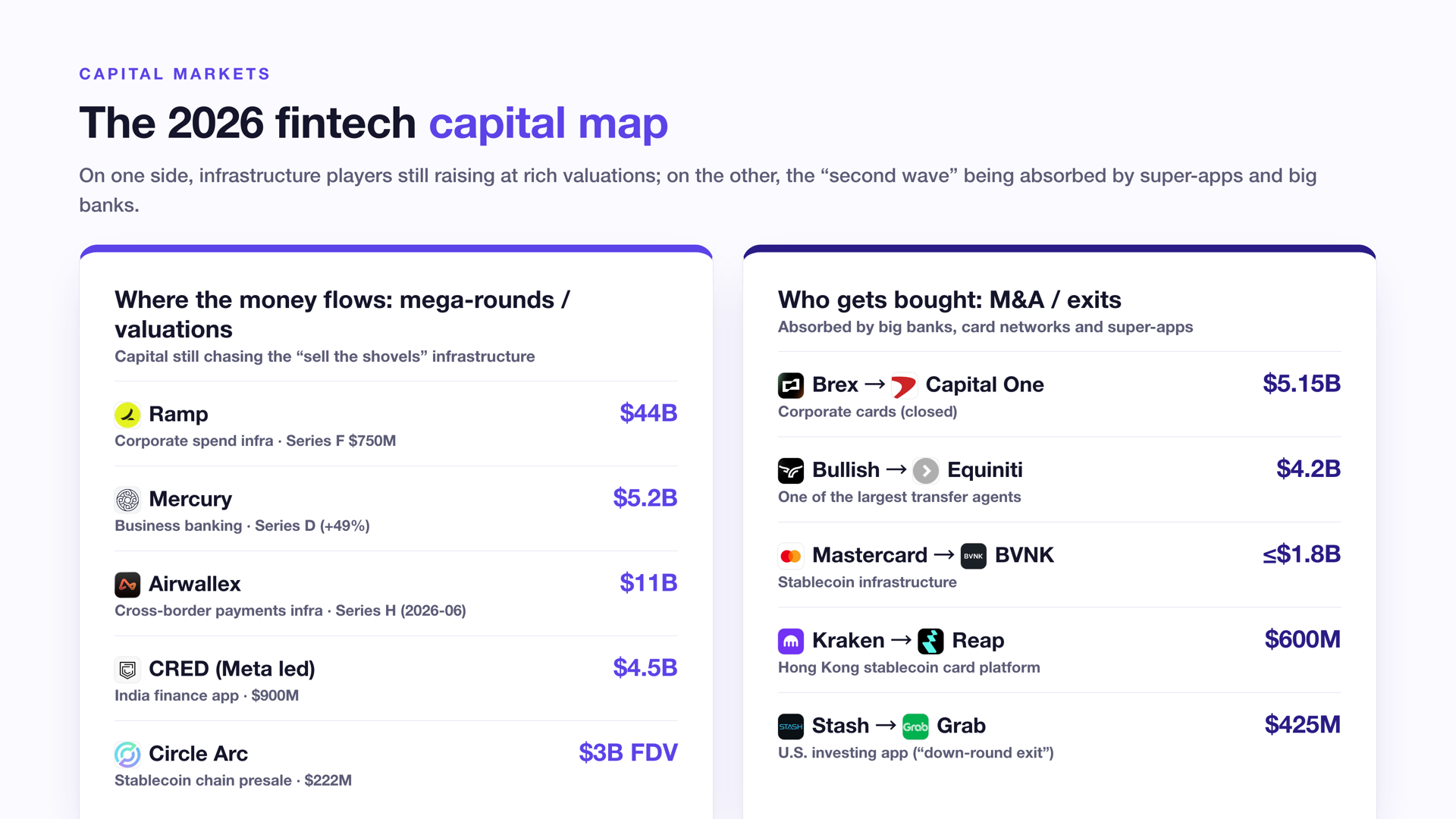

美国的退出生态像一张密织的网,条条是路。光是这一两年,我们就看到:Brex 被 Capital One 以 51.5 亿美元收购(已交割);Bullish 以 42 亿美元买下转让代理 Equiniti;Kraken 母公司花 6 亿美元买下香港稳定币卡平台 Reap。就算并购失败也死不了人——Adobe 200 亿美元收购 Figma 因反垄断告吹、赔了 10 亿分手费,Figma 转头自己独立 IPO。在美国,被大行收、被卡组织收、被同行整合、或者干脆自己上市,是一套成熟到「失败了也能全身而退」的退出生态。

最贴切的注脚,是 Stash 的故事。2026 年 2 月,东南亚超级 App Grab 以 4.25 亿美元企业估值收购了美国投资 App Stash(先拿 50.1% 股权,剩下的三年内按公允价值收齐)。Grab 买的不是 Stash 的代码,是它现成的「48 州监管框架 + 50 亿美元 AUM + 100 万付费订阅用户」——省下自己从零搭一套美国金融基建的时间。

但 Stash 这个案例还有一层更冷的真相,简直是为这一篇量身定做的:Stash 累计融了约 7.47 亿美元,4.25 亿的退出其实是一笔「水下退出」——晚期投资人要打折、普通股基本归零。同一时期,连 MrBeast 的公司都收购了青少年银行 Step。这批「第二波 neobank」够不到 Revolut 那种 IPO 逃逸速度,只能按「对超级 App 还有多少工具价值」被重新定价、被收编。

把镜头转回中国,对比是刺眼的:A 股对这类公司并不友好,海外上市的窗口时开时关,产业并购也远不如美国活跃;最有标志性的一幕,是蚂蚁集团 2020 年那场史上最大 IPO,在最后关头被叫停。退出生态一旦薄,敢押十年长线基建的耐心资本就少——而 Stripe、Airwallex 这种公司,恰恰需要十年的耐心。

顺带说一句,美国的退出生态还有一个反直觉的特征:最强的金融基建反而不上市。全球前三大资管里有两家是私有的——Fidelity 由家族持股、Vanguard 由客户共同所有、Capital Group 由员工合伙持有。它们不被季度财报绑架,可以下注最长的周期。这种「私人巨头」的形态,在中国的金融体系里几乎不存在。

美国资本市场的纵深,还体现在它给「退出」留足了形态。一边是 IPO 越来越晚、越来越只服务内部人——SpaceX 上市时,有人感叹「对一个普通美国人来说,你买到它股票的第一次机会,是在 2 万亿美元估值的时候」;另一边,连私募信贷这种另类资产都向散户开了口子(尽管 2026 年一季度散户集中赎回,多只 semi-liquid 基金同时触发限赎,高盛也预计未来两年 private credit 将持续净流出——繁荣里也藏着脆弱)。但不管形态怎样,美国给资本准备了一整套「进得去、也出得来」的管道;管道越多越畅通,敢在早期押注十年长跑的耐心资本就越多。这正是 Stripe、Airwallex 这种「要烧十年」的公司,最需要的那种底层条件。

更别说资本市场的深度,中美根本不在一个量级。美股的池子深到什么程度?它能一口气吞下 SpaceX 这种两万亿美元的巨无霸 IPO,流动性连个涟漪都不起——哪怕同时再来一个两万亿,也照样接得住。港股呢?别说两万亿,连一个字节跳动都接不住:真要让字节这个体量的盘子在港股上市流通,整个市场的流动性会被瞬间抽干。退出这条路,不光要有人接盘(并购),还得有个深到能容下大船的港口(资本市场)——美国两样都有,中国两样都薄。这也是为什么同样是「烧十年」,钱敢投在美国,不敢投在这边。

五、压在土壤之上的:监管,与那条美元轨道

四块土壤之外,还压着一层更硬的东西——监管对「竞争」的态度。

一个常被忽略的细节是:美国白宫 2026 年那道金融科技行政令,第一次把「促进竞争、清理阻碍创新的规则」明明白白写进了监管目标。有评论者直言:「在这一刻之前,我不认为监管里存在一个清晰的『促进竞争』的授权。」——连美国都要专门下一道令来鼓励竞争,可见这事多不容易。

而中国这边,方向是反的。2026 年 5 月,证监会等部门对富途、老虎、长桥作出拟处罚的事先告知,认定其非法经营证券业务:富途拟被罚没逾 18.5 亿元人民币、CEO 李华个人被罚 125 万元;老虎合计约 4.11 亿元。这是八部门「两年集中整治非法跨境证券业务」的一部分——2023 年起 App 在内地下架,存量内地客户只准单向卖出、转出,到期全面关停。换句话说,富途最成功的那块业务(服务内地跨境客户),正在被结构性地关上闸门。这恰好呼应了第一篇的结论:富途不是「中国内地长出的 Schwab」,它是一群中国人跑到境外才长出来的全球券商。

最后,还有一条第三篇埋下的暗线:稳定币这条最新的金融轨道,全市场约 99% 是美元。稳定币越成功,越是在全球分发美元。一个靠资本管制守住货币主权的国家,要不要、能不能上这条轨道?这一问,本身就是中美土壤差异最尖锐的一个切片——美国的金融基建天然站在「美元全球分发」的顺风口上,而人民币的轨道,被资本管制这堵墙挡着。

更反直觉的是下面这一幕:明知稳定币已经是美元的天下——全市场约 99% 挂美元、本币加起来不到 1%——亚洲各国这两年还是抢着发自己的。日本 2026 年要上受监管的日元稳定币、只准银行和信托发;香港 2025 年 8 月《稳定币条例》生效,专门给港元稳定币发牌;韩国也在为韩元稳定币立法吵个不停。图什么?图货币主权。逻辑很朴素:要是你国老百姓发工资、存钱、付款都默认用美元稳定币,钱就一点点从本国金融体系漏走——这叫「数字美元化」,是央行最怕的事。还有更实在的一层:今天一笔韩元换日元,底层大概率还绕道美元中转,凭空多一道成本和时延;发本币稳定币,至少想把这道「美元过路费」省下来。说白了,这条轨道你可以不上——但不上,就等于默认把这条最新金融轨道上的货币主权,拱手让给美元。连日、港、韩这些美国盟友,都要在美元轨道旁边费劲铺一条自己的窄轨;中国的答案则更彻底:与其上一条注定分发美元的公共轨道,不如自己搞数字人民币、把稳定币牢牢圈在监管和资本管制里试。同一条最新轨道,美国顺风、亚洲逆风、中国干脆想另修一条——这,就是那条美元暗线在中美土壤上照出的最尖锐分野。

六、Devil’s Advocate:可中国支付明明全球最强,怎么会「出不了 Stripe」?

按惯例,先把唱反调的理由打满,再回到判断。

Bull case,认真地说:要论支付,中国不是落后,是遥遥领先。

中国的移动支付渗透率全球第一,支付宝和微信的二维码,让美国那套「刷卡 + 收单」显得像上个时代的产物。带中国基因的跨境玩家也在全球开疆拓土——Airwallex 能在 110 亿美元估值上融资。靠支付宝分发的余额宝,曾是全球最大的货币基金。富途,更是把 3000 万用户、万亿资产的全球券商做了出来。所以「中国出不了 Stripe」这句话,听着甚至有点傲慢:论支付基建的规模和体验,也许是 Stripe 该向中国学。

替反方再说一句类比:巴西版的 Google 还是 Google,但巴西版的「摩根大通」是 Nubank——在很多市场,本土玩家不是造不出,而是直接把原版拍在了沙滩上。中国的支付,正是这种「本土更强」的样本。

但回到判断:「出不了 Stripe」问的,从来不是「有没有支付公司」。

它问的是:有没有那一层——中立的、面向企业的、靠企业付费意愿和并购退出生态长大的基建。

中国的支付确实更强,但那是面向消费者的钱包入口(支付宝、微信),是 C 端的水龙头;而 Stripe 是 B 端的水管,是开发者几行代码就能调用的中立基建。一个国家可以有全世界最好的水龙头,却没有一家独立的自来水公司——因为水管这层,被两个平台和国家队占满了。

有人会说:支付宝微信不也给商户做收单结算吗?做,但那是水龙头自带的接水盆——费率被压到 0.6% 以下、清算走网联、且永远只服务自己这个闭环。收单的「功能」,中国有的是;收单的「中立基建生意」,一天都没存在过。最能说明问题的是蚂蚁自己的选择:它把最像 Stripe 的两块业务——Antom(全球商户收单)和万里汇(WorldFirst,跨境收款)——装进了总部在新加坡、2024 年起独立运营的蚂蚁国际(Ant International)里,做的全是境外的生意。

更关键的是:中国最成功的那几家金融基建创新——富途、Airwallex——无一例外,都是把战场选在了境外、甚至要主动跟「中国」保持距离,才长起来的。这非但不是反例,反而是最有力的正例:它们最成功的那部分,恰恰是它们跑到中国那片土壤之外,才实现的部分。

七、收口:Stripe 不是一个产品,是一种土壤的产物

用一条线,收束整个系列。

券商和资管的解耦,在美国上一个十年就发生完了,费率归零、无肉可割;于是最聪明的钱掉头去打银行;但打银行消费侧的明星公司大多周期、薄利、烧钱,Chime 上市对折、Klarna 腰斩、消费金融退出遇冷;真正穿越周期、赚到大钱的,是卖铲子的人——Stripe 三年翻盘到 1590 亿、Adyen 守着 53% 的软件级利润率。

而卖铲子的人,是一种土壤的产物。它需要企业愿意为软件付钱,需要一个不被超级 App 垄断入口的市场,需要独立的分销渠道,需要一条能让十年长跑的资本体面退出的路。这四样,美国都有,中国都缺——缺的不是人才,是土壤。

所以「为什么中国出不了 Stripe」,最终的答案是:Stripe 不是一个可以被复制的产品,它是一整片土壤长出来的果实。你能在中国找到比 Stripe 更聪明的工程师、比 Stripe 更好用的支付体验,但你很难在中国,复制出那片让「中立基建」得以独立长大的土壤。

但这不是一个悲观的结尾。富途和 Airwallex 已经指出了一条现实的路:既然那片土壤在中国之外,那就把战场选在土壤更肥的地方。立足香港、辐射东南亚,做 B2B 的嵌入式金融与 agentic 金融轨道,让超级 App 和虚拟银行来当你的分销,最后像 Stash 卖给 Grab 那样、被一个更大的平台体面收编——这是一条已经被验证的、属于中国创业者的「卖铲子」之路。

只是记住一件事:这条路不是「问题不大」,而是一场七到十年、以牌照为护城河的硬仗。能不能扛下来,比的不再是产品,是资本、是时点,是你愿不愿意离那片更肥的土壤更近一点。土壤在哪,人就得往哪挪——这个坎,没人替你过。

这,就是我这个系列想说的全部。

(附:两句私货)

系列该说的都说完了,请允许我越出题目,再说两句私货——都跟「选择」有关。

第一句,关于行业:AI 时代,你要不是 CS/工程背景的创业者,我反而更劝你往 fintech 走、或进一家 fintech 公司。 AI 干的事常被理解反了:它降的是写代码的门槛,现在人人都能让模型拼出个东西;但它没降创业的门槛,反而抬高了——门槛低了、人涌进来了、用的还是同一批模型,做出来高度同质化,竞争只会更狠,很多赛道杀到最后全是大厂的天下。AI 自己就是最典型的例子:真正的超额利润沉在模型层、算力层、芯片层、底层 infra,全是工程主导的硬仗(这不就是「卖铲子」么,只不过换成了 AI 的铲子);而应用层的 α 大概率被一路压薄——门槛越来越低、越来越卷,这周 OpenAI 甩出新旗舰,下周 Anthropic、Google 各自跟上,你追都追不完;底下垫的是同一批模型,差异只剩工程实现,护城河一戳就破。金融正好反过来:它的底层逻辑几乎千年不变——信用、清算、资产配置、利率传导、风险管理,从古代钱庄到现代 Stripe,解决的是同一组问题;而这组问题的解法,不是技术,是转换成本和信任,一旦成了标准,α 巨大、能吃几十年。得跟前三篇接一句、免得你误会:我不是说 fintech 不需要工程——Stripe、Adyen 自己就是顶级工程组织;我是说,fintech 真正的护城河不在代码那层,在信任、牌照、监管沟通、商业模式和结构设计这层,而这层恰好是商科、经济背景的人比纯技术更占优的地方。工程会被 AI 平权,信任和牌照不会。

第二句,关于眼光:大部分人对「该去哪」的判断,比现实慢好几年。 我做过几年招聘,一个扎心的观察是:有战略眼光的大学生,极少。说难听点,学生群体本来就谈不上「眼光」——找工作前期靠的是牛人小圈子里的熟人推荐,你在哪个圈子,比行业实际怎么样更能决定你去哪。结果就是,大学生对市场的认知,普遍比真实情况滞后 2、3 年:一直到 2019 年,还有一堆人觉得百度远好过头条;一直到 2021、2022 年,还认定腾讯、阿里远强于字节;一直到 2024 年,游戏圈里还是那句「有鹅选鹅、无鹅选米」(有腾讯去腾讯,没有就去米哈游);一直到 2023、2024 年,智谱、Kimi 这些最锋利的 AI 新贵,还招不到最强的那批校招生。这个 Gap 背后,一半是学校的限制条件:实习时间被卡死、自主实习的门槛高得离谱;学校里管就业的人一大把,不少自己都没真正就业过,更别提摸清市场的真实温度;什么都往「安全」上靠,却忘了大学生本就是成年人——而往往,那些「不听话」的反倒更有眼光,可学校偏偏更喜欢「听话」的。人的认知怎么改得最快?自己亲眼见过,最好是被现实狠狠「撞」过一次。信息差,落后 2、3 年;价值观,落后 5 到 10 年。

这两句私货,其实是同一件事:看清土壤在哪,然后往那儿挪——早一点,比别人早一点。 这也是我写完这整个系列,给自己的答案。

(本文数据采用 2026 年最新可得口径:软件支出 13 倍来自拾象引 Battery Ventures(2022),中国 SaaS 占比来自 IDC;富途/老虎拟处罚金额来自证监会 2026-05-22 事先告知及财经媒体披露;Stash→Grab 4.25 亿美元收购来自 Grab 投资者公告与 SEC 备案;Brex→Capital One 51.5 亿美元、Cred→Meta 9 亿美元投资、余额宝规模、支付宝/微信支付份额等均来自公开媒体报道与公司披露;Airwallex 牌照数与「中国后门」争议综合自公开报道,部分为指控而非定论。涉及中国企业 ARPU、中小企业寿命等数据口径存在出入,仅作量级参考。日本、香港、韩国本币稳定币进展与「99% 挂美元」口径来自公开报道(HKMA《稳定币条例》2025-08 生效等);文末「私货」中关于大学生认知与招聘市场的判断,为作者本人的从业观察,非统计数据。)

"Why There's No Chinese Stripe" series · Part Four (Finale)

In brief — China has the best payment experience on earth, yet it can't grow a Stripe of its own. This isn't a technology gap, still less a talent gap—Futu and Airwallex proved long ago that Chinese founders can build world-class financial products; they just have to build them offshore. So what's missing? The soil. This piece delivers the final answer to the whole series—and at the end, two pieces of unsolicited personal advice for ordinary readers.

Setting the Stage

In June 2026, Meta did something worth pausing over: it put $900 million into the Indian finance app Cred, at a valuation of around $4.5 billion; almost simultaneously, it installed Cred's founder, Kunal Shah, as WhatsApp's global head.

Cred is no bit player—it serves 17 million Indians and, by transaction count, processes more than 40% of India's credit card bills. But the truly interesting part is Meta's calculation: it wants to turn WhatsApp into India's payment super-app. Yet as of May 2026, WhatsApp Pay's share of India's UPI was still just 0.65%. One commentator nailed the crux in a single line—"WhatsApp is everywhere in Indian commerce, and almost nowhere in Indian finance."

Anyone who knows China will smile knowingly at that sentence. Because it's the mirror image of the Chinese story—except China finished this move long ago: once a super-app fills up a country's commerce gateway, independent financial infrastructure struggles to grow out from under its feet.

Put plainly: India's Google is still Google, but India's "JPMorgan" is becoming WhatsApp. Swap "India / WhatsApp" for "China / WeChat, Alipay, Meituan," and this piece's central question is sitting right in front of you.

Across the first three parts, I walked a complete chain: Part One—the unbundling of U.S. brokerages and asset managers finished long ago, fees fell to zero, no meat left on the bone; Part Two—the smartest money pivoted to attack the banks, but most who went after the consumer side fared badly, and the ones who truly rode out the cycles were the pick-and-shovel sellers; Part Three—enterprise payment infrastructure is the crown jewel, and Stripe, Adyen, and Airwallex each proved that "selling shovels" can be a business with software-grade margins.

But the end of Part Three, with Airwallex—that Chinese-founded specimen—already spoiled the shape of the answer: it could grow to $11 billion, yet had to put its headquarters, its data, and its growth outside China, and even actively keep its distance from the word "China" itself.

This is no accident. In this piece, I answer the series' ultimate question head-on—why can this layer of pick-and-shovel infrastructure grow into a crown jewel in America, yet barely grow at all in China?

My answer: China has never lacked fintech talent or product chops—Futu and Airwallex already proved that. What China lacks is the soil that grows a company like Stripe. That soil is made of four variables: enterprise willingness to pay for software; a unified-but-platform-captured market; independent distribution; and an M&A/exit ecosystem. Let me take them one at a time.

I. Soil Variable One: Whether Enterprises Will Pay for Software

Stripe, Adyen, Ramp—these "shovel sellers" were, at bottom, all raised by the same thing: American enterprises are willing to pay for software and infrastructure.

How lopsided is this? Shixiang once cited a set of numbers from Battery Ventures: total software spend in North America is roughly 13 times that of Greater China (over the same period, U.S. per-capita consumer spending was also about 13 times China's). If you find that yardstick dated, take a newer one: in 2019, China's SaaS market was just $3 billion, 2% of the global total (IDC); by 2025, the composite read from several research houses is still that "the U.S. market is roughly 10 times China's."

More damning is the value per customer. In China, about 60% of small and medium-sized enterprises are still on the fence about digitization, and only 3.2% have reached a genuinely high level of it; and the average lifespan of a Chinese SME is far shorter than an American one—when customers don't live long, software's lifetime value (LTV) can't hold up. The result is that China's enterprise SaaS has spent years marinating in a swamp of "red-ocean low prices and chronic unprofitability," with one study estimating that annual per-customer spending power in the U.S. and China differs by nearly tenfold.

(Plain-language aside: SaaS = enterprise software paid for annually; ARPU = average revenue per customer; LTV = the total value a customer contributes over their entire lifetime. Whether an enterprise keeps paying for software, and how long it survives, directly decides whether the shovel sellers get to eat.)

Shixiang put it well: "SaaS is a robot for white-collar workers." In America, software is an essential purchase for enterprises—the billboards lining Silicon Valley's highways are almost all SaaS companies advertising; in China, software is more of a "cut-it-if-you-can" cost line.

This gap in willingness to pay, landing on a single company, is staggering: in America, a decent enterprise software company can have a single large customer contribute tens of millions of dollars a year in recurring revenue—the data-warehouse company Snowflake's big client Capital One contributed tens of millions annually all by itself (per its early prospectus). It is precisely this rich soil—enterprises willing to keep paying for software—that grew Stripe, grew Adyen, and grew that entire row of "shovel sellers" from the previous part's table. Conversely, when a market's enterprises haggle even over software subscriptions and, on average, don't survive a few years, companies in this row can only subsidize, burn cash, and chase ever more downmarket traffic—they simply can't accumulate the kind of repeatable, self-expanding revenue that "selling shovels" requires.

No enterprise willingness to pay, no revenue soil for a Stripe. A company can build beautiful payments, but if no one will keep paying for "beautiful infrastructure," it won't grow into a crown jewel—it can only subsidize, burn cash, and fight for consumer traffic. This is the fated starting point of Chinese fintech.

II. Soil Variable Two: A Unified Market, but One Eaten Clean by Two Platforms

Someone will object: China's market is huge and unified—isn't that the perfect hotbed for a Stripe?

Quite the opposite. China's "unified market" is genuinely unified and genuinely large—but that unity was monopolized into being by two super-apps, not paved by a layer of neutral infrastructure.

Look at payments: Alipay and WeChat Pay together hold over 90% of China's mobile payments. Look at wealth management: on the back of Alipay's distribution, Yu'e Bao was briefly the world's largest money-market fund in 2017–2018, peaking at around ¥1.69 trillion (roughly $268 billion)—it proved China can conjure a giant financial player out of thin air, but the winner was the platform holding the users (Alipay), not some independent asset-management startup.

Nothing illustrates the point better than restaurant SaaS. In America, a company like Toast can grow up independently: starting from restaurant POS, embedding payments into the software stack, collecting SaaS subscription fees on one side and payment take-rates on the other, and growing into a public company.

Here I have to correct a popular claim. People often say "the reason there's no Toast in China is that Meituan embedded it and killed it off." The precise fact is this: Meituan in China built its own restaurant POS from the start (smart terminals, scan-to-order), bundling this vertical SaaS layer together with fulfillment and ad traffic into its own operation; it even went abroad in reverse, assembling a team to build a direct Toast rival called Peppr—which, because Meituan was unwilling to pour money into an overseas war, has already been shut down in the U.S. The in-and-out tells the whole story: in China, the restaurant-SaaS layer simply leaves no crack for independent players; and the super-app's playbook, transplanted to an America without a traffic monopoly, doesn't take to the soil.

This is the paradox of China's "unified market": the market is big enough, but every vertical opportunity—payments, credit, wealth management, restaurant SaaS—gets casually eaten at the gateway layer by Alipay, WeChat, and Meituan using ready-made traffic. An independent Stripe, an independent Plaid, an independent Toast can't find the crack to grow up on its own in a landscape where two super-apps fill every gateway.

Look one layer deeper: the reason super-apps can pick off vertical opportunities one by one isn't how good their products are—it's the thing in their hands that no one else has: ready-made traffic in the billions. An independent startup has to spend years and burn big money to acquire customers, whereas WeChat, Alipay, and Meituan need only add an entry point inside their own apps to casually do credit, wealth management, and restaurant SaaS, at a marginal customer-acquisition cost of nearly zero. This is exactly India's script: WhatsApp dares to dream of doing payments precisely because of its dominant penetration in Indian commerce, not because WhatsApp Pay itself is any good. When distribution can be handed out free via traffic, the road of independent infrastructure—crawling up slowly on product and licenses—looks both slow and unnecessary. This is the most counterintuitive thing about a super-app market: the bigger the market and the stronger the platforms, the smaller the crack left for independent, neutral infrastructure.

III. Soil Variable Three: Independent Distribution, and the Impossibility of "Building a New Network"

The third patch of soil is independent distribution channels and network moats.

As I said last time, the shovel sellers' real moat isn't technology—it's distribution and licenses. Here's a judgment that could serve as the whole series' thesis line: since Discover was born in 1985, no one in America has built a new payment network at retail scale—and that's unlikely to change. And Discover succeeded back then precisely because it rode the distribution of Sears, at the time America's largest retailer.

The barrier in payments also shows up in the layered nesting of licenses—someone likened it to a "Russian doll": open up one payment company and there's another nested inside, all propped up by licenses across jurisdictions; even the largest banks hold direct licenses in only around 60 markets.

A one-line analogy (echoing the whole series): a bank's core system is the bank's pickaxe; enterprise payment infrastructure is the pickaxe of the entire digital economy. Whoever sells the pickaxes stands upstream of every prospector.

So who holds China's "pickaxe"? The answer: no independent third party. UnionPay is the state team's clearing network; WeChat and Alipay are the closed loops of Tencent's and Alibaba's respective traffic platforms. In a market where the distribution gateways are filled up by the state team and the super-apps, a Stripe-like "neutral, developer-facing third-party infrastructure layer grown on enterprise payment" has never lacked technology—what it lacks is the independent-distribution soil it needs to grow.

Say it one layer more bluntly: America's fee-pool chain is commercialized—the card issuer is a commercial bank, the clearer is a listed company like Visa/Mastercard, every segment carries profit and can each be pried loose by a slicker third party. Stripe pried its way in from the "acquiring" segment. And China's chain? The issuing banks are state-owned, the clearer UnionPay is built by the state team, and the gateways are Tencent's and Alibaba's respective closed loops—from end to end, everything is either state or platform; no segment is left as a commercial fee pool for a "neutral third party." This is a more root-level layer than "the market is eaten clean": in America, the fee pool is a commercial cake that can be pried at; in China, it was never a cake open to outsiders at all.

Airwallex's solution is itself proof of this conclusion: it didn't go toe-to-toe inside China, but chose its battlefield in cross-border and overseas markets, laying a network outside China over nearly a decade with 85+ licenses. It even wants to move its staff and data out of China, and has to answer accusations of a "China backdoor"—Keith Rabois, a Khosla partner who also sits on the board of rival Ramp, publicly alleged that its China team and Chinese investors may leave it "obligated to hand over customer data," and U.S. senators have already called for an investigation. A global infrastructure company with Chinese DNA, to grow up, must first prove it is far enough from China.

IV. Soil Variable Four: The M&A and Exit Ecosystem—America Even Made "Getting Acquired" Dignified

The fourth patch of soil, and the most underrated: whether there's a path for a startup to exit with dignity.

America's exit ecosystem is like a densely woven net—every strand a road. In just the last year or two, we've seen: Brex acquired by Capital One for $5.15 billion (closed); Bullish buying transfer agent Equiniti for $4.2 billion; Kraken's parent spending $600 million to buy Hong Kong stablecoin-card platform Reap. Even a failed acquisition isn't fatal—Adobe's $20 billion purchase of Figma collapsed on antitrust grounds and cost a $1 billion breakup fee, and Figma turned around and IPO'd independently. In America, getting bought by a big bank, by a card network, being consolidated by a peer, or simply going public yourself is an exit ecosystem so mature that "even failure lets you walk away whole."

The most fitting footnote is Stash's story. In February 2026, Southeast Asian super-app Grab acquired the U.S. investing app Stash at a $425 million enterprise value (first taking 50.1% of equity, with the rest collected at fair value within three years). What Grab bought wasn't Stash's code—it was its ready-made "48-state regulatory framework + $5 billion AUM + 1 million paying subscribers"—saving itself the time of building a U.S. financial-infrastructure stack from scratch.

But this Stash case has a colder truth underneath, practically tailor-made for this piece: Stash raised roughly $747 million in total, so the $425 million exit was actually an "underwater exit"—late-stage investors took a haircut and common stock went essentially to zero. Around the same time, even MrBeast's company acquired the teen bank Step. This batch of "second-wave neobanks" can't reach the IPO escape velocity of a Revolut, and can only be repriced and absorbed according to "how much tool-value they still hold for a super-app."

Turn the lens back to China, and the contrast is glaring: the A-share market isn't friendly to these companies, the window for overseas listings opens and shuts, and industrial M&A is far less active than in America; the most emblematic scene of all was Ant Group's largest-ever IPO in 2020, halted at the final moment. Once the exit ecosystem is thin, there's less patient capital willing to bet on ten-year-long infrastructure—and companies like Stripe and Airwallex need precisely a decade of patience.

By the way, America's exit ecosystem has a counterintuitive feature: the strongest financial infrastructure actually stays private. Two of the world's three largest asset managers are private—Fidelity is family-held, Vanguard is mutually owned by its clients, Capital Group is held in partnership by its employees. Unshackled from quarterly earnings, they can bet on the longest cycles. This "private giant" form barely exists in China's financial system.

The depth of American capital markets also shows in how much room it leaves for different exit forms. On one side, IPOs come ever later and ever more exclusively serve insiders—when SpaceX went public, someone lamented that "for an ordinary American, your first chance to buy the stock is at a $2 trillion valuation"; on the other side, even an alternative asset like private credit has opened a door to retail investors (though in Q1 2026 retail redemptions clustered, several semi-liquid funds hit redemption gates at once, and Goldman Sachs expects private credit to keep seeing net outflows over the next two years—there's fragility hidden inside the boom, too). But whatever the form, America has prepared a full set of pipes that "let you in and let you out"; the more numerous and free-flowing the pipes, the more patient capital dares to bet early on a ten-year run. This is exactly the foundational condition that companies like Stripe and Airwallex—the ones that "have to burn for a decade"—need most.

Not to mention that the depth of the capital markets isn't remotely in the same league. How deep is the U.S. equity pool? It can swallow a $2 trillion behemoth IPO like SpaceX in one gulp without even a ripple of liquidity—even if a second $2 trillion came at the same time, it would take that too. Hong Kong? Forget $2 trillion—it can't even take a single ByteDance: actually floating a book the size of ByteDance on the Hong Kong exchange would instantly drain the entire market's liquidity. An exit needs not only a buyer (M&A) but also a harbor deep enough to hold a big ship (capital markets)—America has both, China is thin on both. That's why, for the same "ten-year burn," money dares to invest in America but not over here.

V. Pressing Down on the Soil: Regulation, and That Dollar Rail

Beyond the four patches of soil, there's a harder layer pressing down—regulation's attitude toward "competition."

An often-overlooked detail: the White House's 2026 fintech executive order was the first to write "promote competition, clear away rules that obstruct innovation" plainly into the regulatory objectives. As one commentator put it bluntly: "Before this moment, I don't think there existed a clear 'promote competition' mandate in regulation." That even America has to issue an order specifically to encourage competition shows how hard the thing is.

In China, the direction is reversed. In May 2026, the CSRC and other agencies issued advance notice of proposed penalties against Futu, Tiger, and Longbridge, finding them guilty of illegally operating securities businesses: Futu faces a fine and disgorgement of over ¥1.85 billion, with CEO Leaf Li personally fined ¥1.25 million; Tiger, about ¥411 million in total. This is part of an eight-agency "two-year concentrated crackdown on illegal cross-border securities business"—apps have been pulled from mainland stores since 2023, existing mainland clients are permitted only to sell and transfer out one-way, and everything winds down entirely at maturity. In other words, Futu's most successful line of business (serving mainland cross-border clients) is being structurally sealed shut. This echoes exactly the conclusion of Part One: Futu is not "a Schwab grown in mainland China"—it's a global brokerage that a group of Chinese people had to go offshore to grow.

Finally, there's a hidden thread laid down in Part Three: on the newest financial rail—stablecoins—about 99% of the entire market is dollar-denominated. The more successful stablecoins are, the more they distribute dollars globally. Should—and can—a country that guards its monetary sovereignty through capital controls get on this rail? That question is itself one of the sharpest slices of the U.S.–China soil difference: America's financial infrastructure naturally stands in the tailwind of "global dollar distribution," while the RMB's rail is blocked by the wall of capital controls.

Even more counterintuitive is the scene below: knowing full well that stablecoins are already a dollar world—about 99% of the whole market pegged to the dollar, all local currencies together under 1%—Asian countries have still scrambled these past couple of years to issue their own. Japan will launch a regulated yen stablecoin in 2026, issuable only by banks and trusts; Hong Kong's Stablecoins Ordinance took effect in August 2025, purpose-built to license Hong Kong dollar stablecoins; South Korea is still bickering endlessly over legislation for a won stablecoin. What's the point? Monetary sovereignty. The logic is plain: if your citizens default to dollar stablecoins for their paychecks, savings, and payments, money leaks bit by bit out of the domestic financial system—this is "digital dollarization," a central bank's greatest fear. And there's a more concrete layer: a won-to-yen conversion today probably still detours through the dollar under the hood, adding a needless layer of cost and latency; issuing a local-currency stablecoin at least tries to save this "dollar toll." Put bluntly, you can decline to get on this rail—but declining means, by default, handing the monetary sovereignty on this newest financial rail over to the dollar. Even U.S. allies like Japan, Hong Kong, and South Korea are painstakingly laying their own narrow-gauge track beside the dollar rail; China's answer is more thorough still: rather than get on a public rail destined to distribute dollars, build the digital RMB (e-CNY) itself and pilot stablecoins firmly fenced inside regulation and capital controls. On the same newest rail, America has a tailwind, Asia a headwind, and China simply wants to lay a separate track—this is the sharpest divide that dollar thread casts on U.S.–China soil.

VI. Devil's Advocate: But China's Payments Are Clearly the World's Best—How Can It "Not Make a Stripe"?

As usual, let me steelman the counterargument in full before returning to the verdict.

The bull case, in earnest: when it comes to payments, China isn't behind—it's far ahead.

China's mobile-payment penetration is the highest in the world, and Alipay's and WeChat's QR codes make America's "swipe-a-card-plus-acquiring" setup look like a relic of the last era. Cross-border players with Chinese DNA are conquering territory worldwide, too—Airwallex can raise at an $11 billion valuation. Yu'e Bao, distributed via Alipay, was once the world's largest money-market fund. And Futu built a global brokerage with 30 million users and trillions in assets. So the line "China can't make a Stripe" even sounds a little arrogant: in scale and experience of payment infrastructure, maybe it's Stripe that should learn from China.

Let me offer one more analogy for the other side: Brazil's Google is still Google, but Brazil's "JPMorgan" is Nubank—in many markets, local players don't just fail to build the original; they slam the original onto the beach. China's payments are exactly this "the local version is stronger" specimen.

But back to the verdict: "can't make a Stripe" was never asking "is there a payment company."

It's asking: is there that one layer—the neutral, enterprise-facing infrastructure grown on enterprise willingness to pay and on an M&A/exit ecosystem.

China's payments really are stronger, but that's the consumer-facing wallet gateway (Alipay, WeChat)—the consumer-side faucet; whereas Stripe is the B-side pipe, neutral infrastructure a developer can call with a few lines of code. A country can have the best faucet in the world and still not have a single independent water utility—because the pipe layer is filled up by two platforms and the state team.

Someone will say: don't Alipay and WeChat do acquiring and settlement for merchants too? They do, but that's the faucet's built-in catch basin—rates squeezed below 0.6%, clearing routed through NetsUnion, and it only ever serves its own closed loop. The "function" of acquiring, China has in abundance; the "neutral-infrastructure business" of acquiring has never existed for a single day. Nothing illustrates the point better than Ant's own choice: it packed the two businesses most like Stripe—Antom (global merchant acquiring) and WorldFirst (cross-border collections)—into Ant International, headquartered in Singapore and independently operated since 2024, doing entirely offshore business.

More crucially: China's most successful financial-infrastructure innovations—Futu, Airwallex—without exception chose their battlefield offshore, even actively keeping their distance from "China," in order to grow. Far from being counterexamples, they're the most powerful positive examples: the very part of them that succeeded most is precisely the part they realized only by going outside China's soil.

VII. Closing the Loop: Stripe Isn't a Product, It's the Product of a Soil

Let me draw one line to bind the whole series together.

The unbundling of brokerages and asset managers finished in America's last decade, fees fell to zero, no meat left on the bone; so the smartest money pivoted to attack the banks; but most of the star companies going after the banks' consumer side were cyclical, thin-margined, cash-burning—Chime's IPO halved, Klarna was cut in half, consumer-finance exits met a cold reception; the ones who truly rode out the cycles and made the big money were the shovel sellers—Stripe clawed back from three years to $159 billion, Adyen holding a software-grade 53% profit margin.

And the shovel seller is the product of a soil. It needs enterprises willing to pay for software, a market whose gateways aren't monopolized by super-apps, independent distribution channels, and a road that lets a decade-long run of capital exit with dignity. America has all four; China lacks all four—what's missing isn't talent, it's soil.

So the final answer to "why there's no Chinese Stripe" is: Stripe isn't a product that can be copied; it's the fruit grown by a whole patch of soil. You can find engineers in China smarter than Stripe's, and a payment experience more usable than Stripe's, but you'll struggle to replicate, in China, the soil that lets "neutral infrastructure" grow up independently.

But this isn't a pessimistic ending. Futu and Airwallex have already pointed to a realistic path: since that soil is outside China, choose your battlefield where the soil is richer. Base yourself in Hong Kong, radiate across Southeast Asia, build B2B embedded finance and agentic financial rails, let the super-apps and virtual banks be your distribution, and in the end get absorbed with dignity by a bigger platform—the way Stash sold to Grab. This is an already-proven "shovel-selling" road that belongs to Chinese founders.

Just remember one thing: this road isn't "no big deal"—it's a seven-to-ten-year hard fight with licenses as the moat. Whether you can endure it is no longer a contest of product; it's a contest of capital, of timing, of whether you're willing to move a little closer to that richer soil. Wherever the soil is, that's where people must move—this is a hurdle no one can clear for you.

That is everything I set out to say in this series.

(Postscript: two pieces of unsolicited advice)

The series has said what it needed to; allow me to step outside the topic and add two pieces of personal advice—both about "choices."

First, about the industry: In the AI era, if you're not a founder with a CS/engineering background, I'd actually urge you toward fintech—or into a fintech company. What AI does is often understood backwards: it lowers the barrier to writing code—now anyone can get a model to bolt something together; but it hasn't lowered the barrier to starting a company, it's raised it. The barrier drops, people pour in, everyone's using the same batch of models, and what comes out is highly homogeneous, so competition only gets fiercer, and many arenas end up entirely as the giants' domain. AI itself is the most typical example: the real excess profit settles in the model layer, the compute layer, the chip layer, the underlying infra—all engineering-led hard fights (isn't that just "selling shovels," only swapped for AI's shovels?); whereas the alpha at the application layer will most likely be ground thin all the way down—the barrier keeps dropping, keeps getting more crowded; this week OpenAI throws out a new flagship, next week Anthropic and Google each follow, and you can't even keep up chasing; underneath it all lies the same batch of models, the only difference left is engineering implementation, and the moat breaks at a poke. Finance is exactly the reverse: its underlying logic has barely changed in a thousand years—credit, clearing, asset allocation, interest-rate transmission, risk management, from ancient money houses to modern Stripe, it solves the same set of problems; and the solution to that set of problems is not technology, but switching costs and trust—once it becomes a standard, the alpha is enormous and can be eaten for decades. I have to add a line to connect with the first three parts, lest you misread me: I'm not saying fintech doesn't need engineering—Stripe and Adyen are themselves top-tier engineering organizations; I'm saying that fintech's real moat isn't at the code layer, it's at the layer of trust, licenses, regulatory communication, business model, and structural design—and that layer is precisely where people with business and economics backgrounds have the edge over the purely technical. Engineering will be equalized by AI; trust and licenses won't.

Second, about foresight: Most people's judgment of "where to go" lags reality by several years. I did recruiting for a few years, and one painful observation is: college students with strategic foresight are exceedingly rare. To put it harshly, the student cohort can hardly be said to have "foresight" at all—early on, job-hunting relies on referrals within small circles of high-flyers, and which circle you're in determines where you go more than how the industry is actually doing. The result is that students' read on the market generally lags reality by 2–3 years: all the way to 2019, a whole crowd still thought Baidu was far better than Toutiao; all the way to 2021–2022, they still held that Tencent and Alibaba were far stronger than ByteDance; all the way to 2024, the gaming world still repeated "if there's Goose, pick Goose; if not, pick Mihoyo" (if there's Tencent, go to Tencent; if not, go to Mihoyo); all the way to 2023–2024, the sharpest AI upstarts—Zhipu, Kimi—still couldn't recruit the strongest campus hires. Behind this gap, half is the schools' constraints: internship time is capped, the bar for arranging your own internship is absurdly high; schools are full of people managing job placement, many of whom have never truly held a job, let alone gauged the real temperature of the market; everything leans toward "safe," while forgetting that college students are adults to begin with—and it's often the "disobedient" ones who have more foresight, yet schools happen to prefer the "obedient." How does a person's understanding change fastest? By seeing it with your own eyes—ideally after reality has "slammed" into you once. The information gap lags 2–3 years; the values gap lags 5 to 10.

These two pieces of personal advice are really the same thing: see where the soil is, then move there—a little earlier, a little earlier than everyone else. This, too, is the answer I gave myself after finishing this whole series.

(Note: this piece uses the latest available 2026 figures: the 13x software-spend figure is from Shixiang citing Battery Ventures (2022), China's SaaS share from IDC; the proposed penalty amounts for Futu/Tiger are from the CSRC's advance notice of 2026-05-22 and financial-media disclosures; the Stash→Grab $425 million acquisition is from Grab's investor announcement and SEC filings; the Brex→Capital One $5.15 billion, Cred→Meta $900 million investment, Yu'e Bao's scale, and Alipay/WeChat Pay shares are all from public media reports and company disclosures; Airwallex's license count and the "China backdoor" controversy are synthesized from public reporting, some of it allegation rather than settled fact. Data caliber for Chinese firms' ARPU, SME lifespan, and the like varies across sources and serves only as an order-of-magnitude reference. Progress on Japanese, Hong Kong, and South Korean local-currency stablecoins and the "99% pegged to the dollar" figure are from public reporting (the HKMA Stablecoins Ordinance took effect in 2025-08, etc.); the closing "personal advice" judgments about student perception and the recruiting market are the author's own professional observations, not statistical data.)